No edit summary |

|||

| (11 intermediate revisions by the same user not shown) | |||

| Line 1: | Line 1: | ||

=Bad Debt Relief/Recovered= | |||

# GST registered person is eligble to claim the bad debt relief even if it spans on or after '''1 September 2018'''. | # GST registered person is eligble to claim the bad debt relief even if it spans on or after '''1 September 2018'''. | ||

# Bad Debt Relief is allowed to be claimed '''within 120 days from the SST effective date (eg. 1 September 2018)'''. | # Bad Debt Relief is allowed to be claimed '''within 120 days from the SST effective date (eg. 1 September 2018)'''. | ||

| Line 8: | Line 8: | ||

<br /> | <br /> | ||

==Final GST Return Processor== | |||

''Menu: SST/GST | New GST Return...'' | ''Menu: SST/GST | New GST Return...'' | ||

::[[File:GSTSST-Transitional_02.jpg]] | ::[[File:GSTSST-Transitional_02.jpg]] | ||

<br /> | <br /> | ||

:1. System will AUTO define the last taxable period (A), eg... | :1. System will AUTO define the last taxable period '''(A)''', eg... | ||

::{| class="wikitable" border="1" | ::{| class="wikitable" border="1" | ||

|- | |- | ||

| Line 23: | Line 23: | ||

<br /> | <br /> | ||

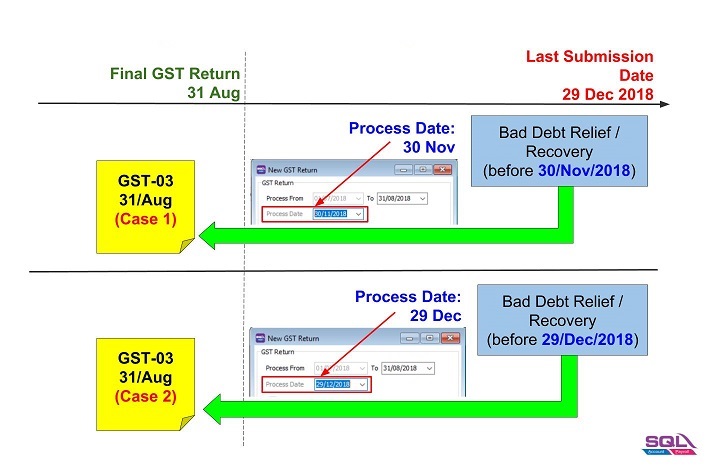

:2. Set the Process Date | :2. Set the Process Date '''(B)''' as the date submit the Final GST return before 29 December 2018 (within 120 days from the SST effective date). | ||

:For example, | ::a) For example, | ||

:: | ::[[File:GSTSST-Transitional_03.jpg | 1000PX]] | ||

| | <br /> | ||

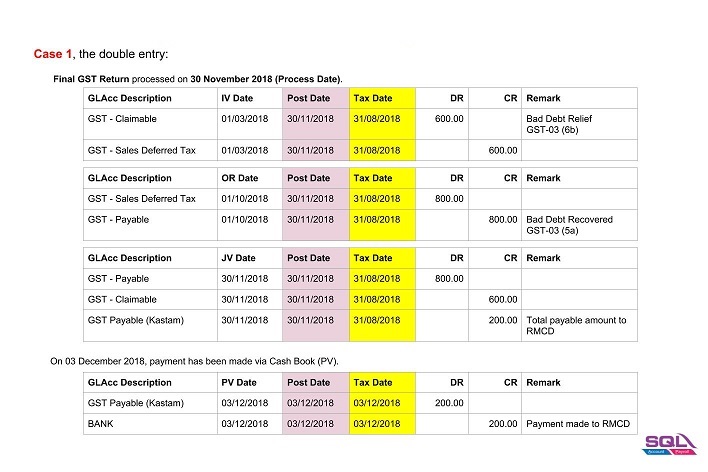

::b) Double entry for '''Cases 1'''. | |||

::[[File:GSTSST-Transitional_04.jpg | 1000PX]] | |||

| | <br /> | ||

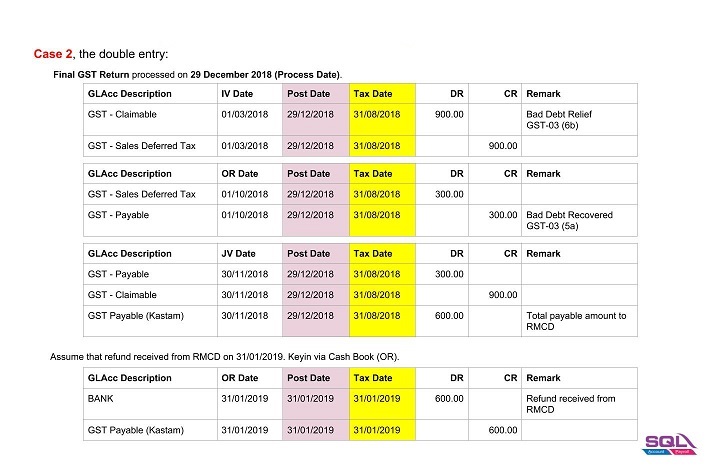

::C) Double entry for '''Cases 2'''. | |||

::[[File:GSTSST-Transitional_05.jpg | 1000PX]] | |||

<br /> | |||

=Retention Invoice Payment= | |||

==See also== | ==See also== | ||

Latest revision as of 04:00, 11 October 2018

Bad Debt Relief/Recovered

- GST registered person is eligble to claim the bad debt relief even if it spans on or after 1 September 2018.

- Bad Debt Relief is allowed to be claimed within 120 days from the SST effective date (eg. 1 September 2018).

- Bad Debt Recovery made on or after 1 September 2018 must to be paid as output tax to RMCD within 120 days from the SST effective date by amending the Final GST Return.

Final GST Return Processor

Menu: SST/GST | New GST Return...

- 1. System will AUTO define the last taxable period (A), eg...

Process From Process To 01/07/2018 31/08/2018

- 2. Set the Process Date (B) as the date submit the Final GST return before 29 December 2018 (within 120 days from the SST effective date).

- a) For example,

- b) Double entry for Cases 1.

- C) Double entry for Cases 2.